Market Commentary

U.S. equity markets began the week on solid footing, shrugging off some of the recent choppiness seen in global markets.

In China, retail sales came in well below expectations, furthering concerns about the trajectory of the world’s third-largest economy. The disappointing data added to a series of lackluster reports, while murky details about additional stimulus have done little to inspire confidence in markets.

In Europe, political and economic turbulence dominated. France’s credit rating was downgraded following a budget dispute that saw far-right leader Marine Le Pen ousting the prime minister, adding fresh uncertainty to the eurozone’s second-largest economy. Meanwhile, Germany faces its own political problems as Chancellor Olaf Scholz is widely expected to lose a critical no-confidence vote later this week. Should that happen, it would likely trigger new elections and add another layer of instability to Europe’s largest economy, which has been stagnant.

Closer to home, the Federal Reserve takes center stage as traders anticipate this week’s rate decision. It is widely expected that the Fed will cut interest rates by another 0.25%. While inflation remains elevated above the central bank’s target and the labor market shows signs of slowing, the Fed is likely to signal a reassessment of its current pace of rate cuts as it looks ahead to 2025. Markets are now pricing in the possibility of three more quarter-point cuts next year, a likelihood that could gain further clarity when the Fed releases its updated rate projections on Wednesday.

Other economic data to keep your eye on this week includes Retail Sales and the PCE index read. Retail sales tracks the demand for consumer goods and is expected to increase 0.6% YoY, accelerating from its previous read last month. Core PCE comes out after the Fed interest rate decision, however it is their preferred gauge of inflation. Expectations are calling for a 2.9% YoY read, up from 2.8% last month.

In U.S. equity markets, there’s been a renewed focus on mega-cap tech names, with traders gravitating back toward these giants after a period of broader market outperformance. It remains to be seen whether this is the start of a longer-term trend favoring these behemoths or merely year-end window dressing. Given this recent theme, breadth has weakened from moderate levels. 50% of stocks are above their 50-day moving average. Higher readings indicate more participation in the average stock.

In fixed income, the recent rally in bonds has cooled, with the 10-year Treasury yield climbing back near 4.4%. This reversal appears driven by stronger economic data, ongoing policy uncertainty, and diminished expectations for future rate cuts.

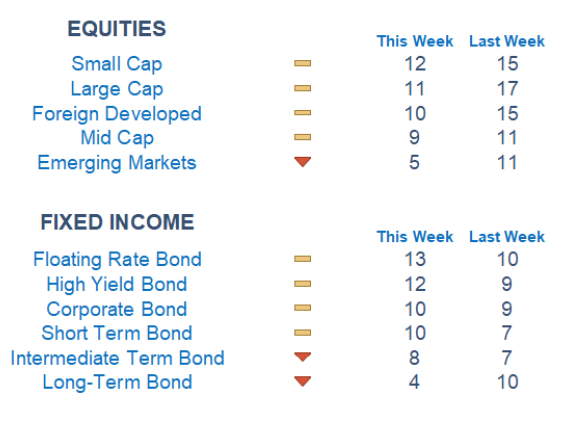

Our Newton models align with many of these themes. Large-cap equities are scoring better than most of their small-cap counterparts, while domestic markets remain more attractive than international ones. In fixed income, the long bond, which is highly sensitive to interest rate movements, continues to score the worst. Conversely, high yield, the segment most correlated with equities, scores the best. Sector performance trends remain mostly consistent, with Communication and Consumer Discretionary scoring the best while Health Care, Materials, and Energy remain weak.

Economic Releases This Week

Monday: Empire State Manufacturing Survey, S&P Flash Services & Manufacturing PMI

Tuesday: US Retail Sales, Home Builder Confidence Index

Wednesday: Housing Starts, FOMC Interest Rate Decision

Thursday: Initial Jobless Claims, GDP (Second Revision), Existing Homes Sales, US Leading Economic Indicators

Friday: PCE Index

Stories to Start the Week

Softbank CEO Masayoshi Son will announce a $100 billion investment in the U.S. over the next four years today at Donald Trump’s residence at Mar-a-Lago.

Honeywell said it was considering a plan to separate its high-margin aerospace business.

Republicans clash over ‘SALT’ deduction as they seek to extend Trump’s tax law.

What is Newton?

Our Newton model attempts to determine the highest probability of future price direction by using advanced algorithmic and high-order mathematical techniques on the current market environment to identify trends in underlying security prices. The Newton model scores securities over multiple time periods on a scale of 0-20 with 0 being the worst and 20 being the best possible score.

Trend & level both matter. For example, a name that moves from an 18 to a 16 would signal a strong level yet slight exhaustion in the trend.

Technical trading models are mathematically driven based upon historical data and trends of domestic and foreign market trading activity, including various industry and sector trading statistics within such markets. Technical trading models, through mathematical algorithms, attempt to identify when markets are likely to increase or decrease and identify appropriate entry and exit points. The primary risk of technical trading models is that historical trends and past performance cannot predict future trends and there is no assurance that the mathematical algorithms employed are designed properly, updated with new data, and can accurately predict future market, industry and sector performance.