S&P 500: 1.57% DOW: 2.32% NASDAQ: 1.88% 10-YR Yield: 4.17%

What Happened?

Busy week from the Oval Office, and an even busier one for the pizza shops tasked with keeping late‑night staffers fed around the Pentagon, Treasury, and everywhere in between. Headlines flew in every direction: a proposed ban on large investment firms buying single‑family homes, fresh jobs data confirming a “low hire, low fire” labor market, and a dramatic turn in Venezuela that puts Washington closer to the spigot of the world’s largest oil reserves. Rather than treating any one of these as a true regime change, indexes largely read them as noisy but ultimately supportive inputs to an already risk‑on backdrop, using the policy drama as just enough fuel to keep the early‑year rally running.

Equities across the board pushed higher, with notable participation from areas outside the usual “Mag 7” leadership as investors leaned into the idea of a broader, more cyclical upswing. The tape stayed anchored by expectations for eventual Fed rate cuts, while softer, but not collapsing, labor data, firming consumer sentiment, and the perception of incremental supply relief on the energy side all helped nudge growth and earnings assumptions in a friendlier direction. In effect, the week’s macro headlines gave markets permission to keep rotating toward a more even rally, without yet forcing a rethink of the prevailing soft‑landing narrative.

Trump Wants to Bar Wall St. Investors From Buying Single-Family Homes

- President Trump announced plans to ban large investment firms from buying single‑family homes.

- Blackstone and other housing‑linked stocks dropped roughly 5–6% on the news.

- Institutional investors own only about 2–4% of U.S. single‑family homes nationally.

The key takeaway – With all the buzz in Washington this week there were many stories to catch-up on, but one announcement in particular grabbed the attention of younger investors and would‑be homebuyers: a plan to ban large investment firms from buying additional single‑family homes in an effort to cool prices and “give houses back to people, not corporations.” Wall Street noticed immediately – shares of Blackstone and other housing‑exposed names sold off around 5–6% as investors tried to handicap what this might mean for one of the market’s favorite real‑asset trades of the last decade. Housing is not just cocktail‑party conversation; it’s roughly one‑sixth of U.S. GDP when you combine construction, remodeling, and housing services like rent and utilities, so any headline threat to that ecosystem gets a quick reaction from macro desks even while the policy details are still sketchy.

On its face, kicking big investors out of the single‑family game sounds like it should open the door for regular buyers, but the catch is scale. Institutional and large corporate owners are estimated to control only a low‑single‑digit share of the U.S. single‑family housing stock – on the order of 2–4% nationally – with heavier pockets of ownership in certain Sun Belt metros, meaning that in many markets Blackstone‑type players simply are not the marginal buyer on the typical Main Street block. That helps explain why most housing economists are pouring cold water on the idea that this ban, if it even makes it through Congress, would materially reshape national home prices: removing one slice of demand does not conjure up new supply; it just changes who is bidding on the same scarce inventory, and in some cases could even chill build‑to‑rent development if large buyers step back. For young buyers hoping this move will suddenly make that three‑bed in a hot zip code affordable, expectations probably need to be tempered; institutions may feel this in their share prices, but with such a small slice of the housing pie, the heavy lifting on affordability will still come from more building, less red tape, and time, making the policy more of a sharp trading headline than a meaningful discount for Main Street.

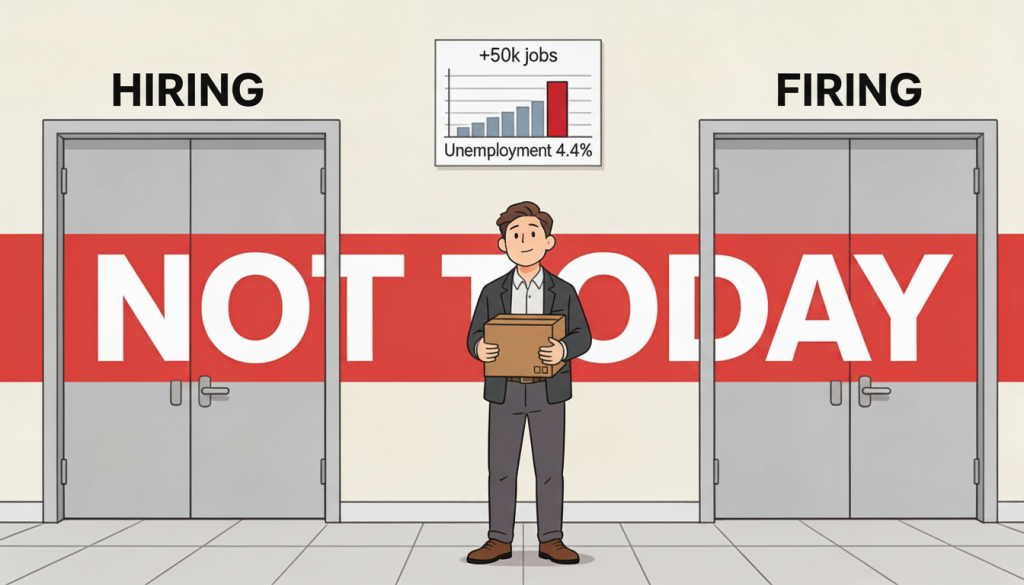

U.S. Job Growth Slows Sharply as Unemployment Ticks Down to 4.4 Percent

- Nonfarm payrolls: +50,000 in December vs. consensus around +55,000–60,000, with earlier months revised lower.

- Unemployment rate: edged down to 4.4% from 4.5% in November.

- Wages: average hourly earnings up 0.3% month‑over‑month and 3.8% year‑over‑year.

The key takeaway – The latest jobs report underscored that the labor market has shifted into a low‑hire, low‑fire gear: employers added just 50,000 jobs in December, capping a year in which monthly payroll gains averaged roughly 49,000 versus 168,000 in 2024. Headline nonfarm payrolls missed expectations (economists were looking for around 55,000–70,000), and prior months were revised down, November was cut to 56,000 and October’s loss was deepened, reinforcing the sense of an economy that is crawling rather than sprinting into 2026. This is the “low hire” side of the story: companies are cautious about expanding headcount but not panicked enough to start large‑scale layoffs, which is exactly the kind of muddling‑through dynamic that tends to keep risk assets on edge without giving anyone a clean recession or recovery narrative.

It was not all bad news, though, which is where the “low fire” piece comes in. The unemployment rate actually ticked down to 4.4% from a revised 4.5% in November, and broader underemployment measures eased as well, suggesting that workers who do have jobs are largely hanging onto them. Wages rose 0.3% on the month and 3.8% year‑over‑year, enough to keep real income growing modestly but not so hot that it forces the Fed back into hawkish mode, leaving policymakers and markets to debate whether this kind of slow‑motion labor market is the perfect soft‑landing backdrop or just the prelude to something weaker later in the year.

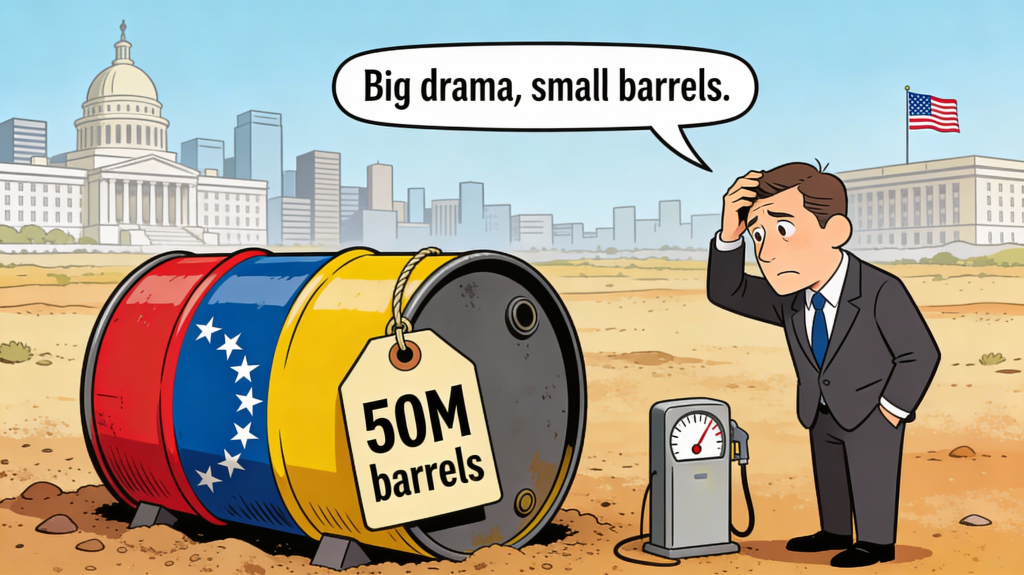

U.S. to get 30 million to 50 million barrels of oil from Venezuela at market price

- Venezuela holds roughly 300 billion barrels of proven crude reserves.

- Trump says the U.S. will refine and sell 30–50 million barrels of Venezuelan crude a year at the high end.

The key takeaway – Oil markets opened the week to a geopolitical twist: President Nicolás Maduro of Venezuela was detained in a U.S.-backed move, and Washington quickly outlined plans to oversee the country’s transition and, crucially, its oil sector “until it can run well on its own.” That headline alone was enough to jolt energy names higher on Monday, helped by reminders that Venezuela sits on the world’s largest proven crude reserves, roughly 300 billion barrels, about one‑fifth of global reserves, even though years of mismanagement and sanctions have left current output stuck well below 1 million barrels per day, a fraction of the more than 3 million barrels it pumped in the late 1990s. Markets initially seized on President Trump’s claim that Venezuela would “turn over” 30–50 million barrels of oil to the U.S. for refining and sale, which at the upper end works out to roughly 130,000 barrels per day for a year—material for Gulf Coast refiners and shipping routes, but still small in the context of a 100‑million‑barrel‑per‑day global market.

As the week went on, analysts helped investors come back to earth. Industry research houses stressed that Venezuela’s upstream and midstream infrastructure is in disrepair, with output already forecast to fall by 200,000–300,000 barrels per day near term even under friendlier political conditions, and any serious ramp‑up requiring years of capex, technical support, and debt workouts with foreign oil firms that still claim billions in unpaid investments. Oil prices reflected that reality more than the rhetoric: Brent and WTI dipped on the initial headlines about extra Venezuelan barrels, then recovered as traders concluded this was a modest re‑routing of supply rather than a wave of new production, leaving the complex still dominated by non‑OPEC growth, OPEC+ policy, and demand worries rather than regime change in Caracas. In short, the U.S. move to effectively steward Venezuela’s oil industry and secure up to 50 million barrels is a long‑term story for reserves and select equities, but in the near term it looks more like a volatility headline than a new anchor for the oil price curve.

From Around the Watercooler

U.S. Forces Seize Fifth Tanker in Campaign to Track Down Venezuelan Oil

Amazon, Google make dueling nuclear investments to power data centers with clean energy

TSMC fourth-quarter revenue jumps 20%, beats forecasts

Supreme Court holds off on Trump tariff ruling for now