MARKET COMMENTARY

Markets opened the week on edge after President Trump unveiled a sweeping set of tariff threats aimed at the EU, Mexico, and Russia. A 30% tariff on EU and Mexican imports is scheduled to take effect August 1st unless deals are struck, while Russia faces the threat of a 100% tariff if it does not halt hostilities in Ukraine within 50 days. These developments follow last week’s announcements targeting Canada, Japan, and copper, contributing to growing concerns over inflation and global trade disruption. Still, markets remained relatively composed, with the Nasdaq closing at a new all-time high and the S&P 500 inching higher, as investors turned their attention to a busy week of earnings and economic releases.

At the top of the economic calendar is Tuesday’s Consumer Price Index (CPI) report, which could set the tone for the week. Economists expect headline CPI to rise 0.2% month-over-month, with core CPI projected at 0.3%, signaling a potential reacceleration in inflation. The year-over-year core inflation figure is expected to edge up to 3%, well above the Fed’s 2% target. This comes as tariff-induced price pressures begin to flow through the economy, particularly in categories like automobiles, building materials, and imported consumer goods. Later in the week, the Fed’s Beige Book will provide anecdotal evidence on economic activity across the country, while June retail sales, due out on Wednesday, will offer a real-time snapshot of consumer strength amid rising prices and rate uncertainty.

Meanwhile, second quarter earnings season begins in earnest with results from JPMorgan, Citigroup, and Bank of America. These reports carry weight given the banks’ role in credit creation and economic intermediation. Analysts will be watching loan growth, net interest margins, and provisions for credit losses, alongside executive commentary on economic trends. JPMorgan’s Jamie Dimon, in particular, often sets the tone with his macro views. The combination of earnings and inflation data could either support or disrupt the market’s recent strength, particularly as equities hover near record highs and Treasury yields creep upward in response to lingering stagflation concerns.

Newton Model Insights:

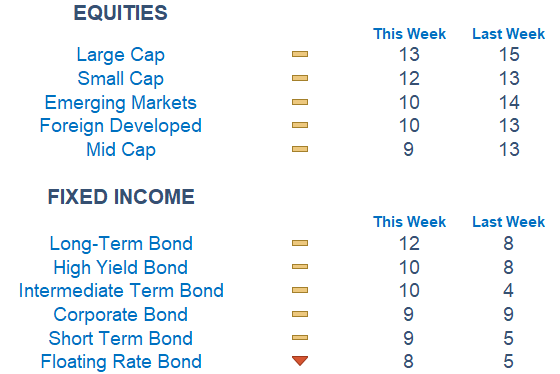

According to our Newton Model, large-cap value has maintained its leadership over mid and small caps for a second week. Domestic equities continue to outperform both foreign developed and emerging markets. Among sectors, materials stand out as the strongest performer, while most others remain weak. In fixed income, long-duration bonds and high yield have taken the lead, though the asset class remains broadly under pressure.

Economic Releases This Week

Monday: None scheduled

Tuesday: Consumer Price Index, Empire State Manufacturing Survey, Dallas Fed Speaks, Big Bank Earnings

Wednesday: Producer Price Index, Industrial Production, Capacity Utilization, Fed Beige Book, New York Fed President Speaks

Thursday: Initial Jobless Claims, US Retail Sales, Import Price Index, Philadelphia Fed Manufacturing Survey, Business Inventories, Home Builder Confidence Index

Friday: Housing Starts, Building Permits, Consumer Sentiment (prelim)

Stories to Start the Week

Trump Raises Pressure on Russia With Tariff Threat, Ukraine Weapons Deal

Nearly One-Third of Major US Housing Markets Now See Falling Home Prices

Bitcoin Climbs to Record $123k as Investors Eye US Policy Boost

Elon Musk Floats a New Source of Funding for xAI: Tesla

Our Newton model attempts to determine the highest probability of future price direction by using advanced algorithmic and high-order mathematical techniques on the current market environment to identify trends in underlying security prices. The Newton model scores securities over multiple time periods on a scale of 0-20 with 0 being the worst and 20 being the best possible score.

Trend & level both matter. For example, a name that moves from an 18 to a 16 would signal a strong level yet slight exhaustion in the trend.

Technical trading models are mathematically driven based upon historical data and trends of domestic and foreign market trading activity, including various industry and sector trading statistics within such markets. Technical trading models, through mathematical algorithms, attempt to identify when markets are likely to increase or decrease and identify appropriate entry and exit points. The primary risk of technical trading models is that historical trends and past performance cannot predict future trends and there is no assurance that the mathematical algorithms employed are designed properly, updated with new data, and can accurately predict future market, industry and sector performance.