S&P 500: 4.49% DOW: 3.16% NASDAQ: 6.84% 10-YR Yield: 4.31%

What Happened?

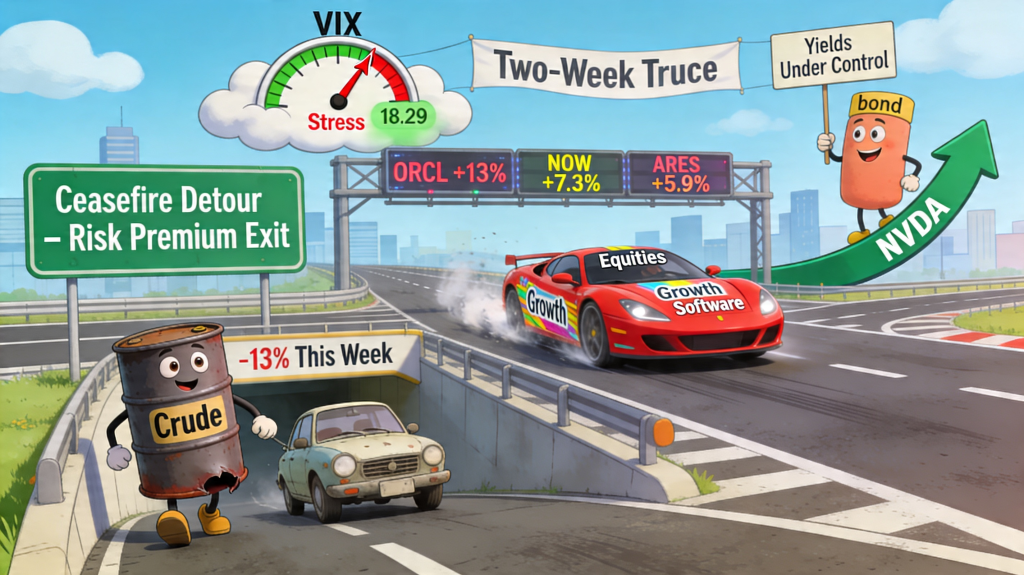

If the last two months of this market were a movie, the plot was simple: oil up, stocks down, repeat. So when a fragile, openly distrusted two-week U.S.-Iran ceasefire took hold on Tuesday, the only real question was how quickly investors would hit “undo” on the war trade. The answer: very. By the closing bell Thursday, the S&P 500 had climbed to 7,041.28, its first close ever above 7,000, and the Nasdaq had notched twelve straight up days, its longest win streak since 2009.

The setup was combustible. Crude had been doing the driving all year, and the market needed just one reason to believe the steering wheel was changing hands. The ceasefire was that reason. Oil shed roughly 13% on the week, Brent slipped back under $96, and the VIX, which had been pushing 22 on Monday, closed Friday at an eerily calm 18.29. That’s the lowest the “fear gauge” has printed since the war began on February 28. Markets can’t rally on headlines alone, but they can absolutely rally on the absence of them.

And then JPMorgan handed them a second reason. Record trading revenue, a comfortable beat on every line, and a shrug of a guidance cut on net interest income. The financial sector, which had spent the better part of March being left for dead, caught fire Tuesday morning and never cooled off. The leadership story went from “nothing works” to “everything works” in about 48 hours, banks on earnings, software on relief, semis on TSMC’s blowout, even the beaten-up names from March’s AI wobble (Oracle, ServiceNow, Ares) ripped higher as short covers unwound.

Not everything was clean. Netflix took a nine-handle haircut in after-hours on Thursday, a reminder that stocks priced for perfection still get punished for anything less. And Cleveland Fed’s Mester used Friday to quietly note that the path to a rate cut still runs through an inflation curve that oil can re-distort at any time. But two back-to-back weekly gains have now erased most of March’s damage — the Nasdaq is up roughly 9% over the fortnight, the S&P up 7%, and the Dow up 6%. Diversified portfolios that stayed the course through the spring drawdown are suddenly looking a lot less underwater, and a lot more like they were supposed to.

The Banks Just Got Paid for Everyone Else’s Anxiety

- JPM trading revenue: $11.6B (+20% YoY) — the largest single quarter in firm history.

- Goldman equities: $5.33B, biggest equities quarter ever; firm-wide $17.23B was second-highest revenue quarter.

- Goldman investment banking fees: $2.84B (+48% YoY), driven by completed-deal advisory revenue.

The key takeaway – For two months, every macro desk on Wall Street has been a 24-hour war room, clients repositioning, hedges rolling, currencies thrashing. Every one of those trades needed someone on the other side. The big banks were that someone, and this week they sent the invoice. JPMorgan’s traders put up the biggest quarter in firm history. Goldman printed its best equities quarter ever. When volatility spikes, the house always wins, and the house is publicly traded.

JPMorgan walked into Tuesday morning with a number that stopped conversation on every trading floor in the country: $11.6 billion in trading revenue, a firm record. Fixed income alone was up 21% year-over-year, driven by exactly the ingredients you’d expect in a quarter shaped by an oil shock — commodities, credit, currencies, and emerging markets. The rest of the P&L came along for the ride, with revenue of $50.5B and EPS of $5.94 comfortably clearing the bar. Even the guidance trim on net interest income (a $1.5B haircut to the 2026 outlook) barely rated a mention; nobody was listening to the lending story while the trading story was this loud.

Goldman had set the tone one day earlier. Equities trading posted a record $5.33 billion, driven by hedge-fund financing that spiked as institutional clients raced to get positioned, or repositioned, as the war unfolded. Investment banking fees jumped 48% on completed-deal M&A work that had been queued up for months. The one note that made veterans raise an eyebrow: Goldman’s provision for credit losses doubled the consensus estimate, the largest reserve build since 2020. Management didn’t elaborate. The market didn’t press. That’s worth filing away.

The broader read is subtle but matters. This wasn’t a “banks are healthy” quarter so much as a “banks are irreplaceable” quarter, the infrastructure that processes a crisis got more valuable because of the crisis. That’s an argument for keeping meaningful financials exposure in diversified portfolios even when headlines suggest banks should be getting hurt. It’s also a reason the broad rotation back into value and cyclical names had so much fuel underneath it this week.

Oil Took an Exit — and the Rest of the Market Followed It Home

- Oil: ~–13% on the week, the largest one-week decline since the war began Feb. 28.

- Brent crude: back near $96 from $108+ three weeks ago; WTI hovering in the low $90s.

- VIX: –18.4% Wed, –7.4% Thu; closed at 18.29 — lowest since the war began.

- Oracle: +13% intraday Monday on AI Customer Edge Summit news.

- Nasdaq: 12 consecutive winning sessions, longest streak since July 2009.

The key takeaway – A two-week ceasefire nobody fully trusts was nonetheless enough to pull oil down 13% on the week, drain the geopolitical premium out of bond yields, and hand leadership right back to the groups that needed it most — growth, software, and semiconductors. The truce may not last. But for one week, the market got to remember what life looks like when it isn’t being dictated by a headline.

The week began with the worst possible setup. On Sunday night, Trump posted on Truth Social that the U.S. Navy would “begin the process of BLOCKADING” the Strait of Hormuz. Futures cratered: Dow –517, S&P –1.1%, Nasdaq –1.2%. Brent was flirting with $100 a barrel, the VIX was back above 21, and Monday morning looked like it would be another entry in the long list of gap-down opens that had defined 2026.

It didn’t happen. By midday Monday, Trump announced “we’ve been called by the other side,” talks resumed, and by Tuesday evening a two-week ceasefire was in place. The response across markets was immediate and correlated. The VIX fell 18.4% on Wednesday, another 7.4% Thursday, and closed the week at 18.29 — the lowest reading since the war began on February 28. Oil gave back roughly 13% over five sessions, the biggest one-week decline of the conflict. The 10-year yield, which had been pricing in inflation scenarios you don’t want to think about, drifted quietly in a 4.26%–4.31% band. Boring bonds and boring energy are exactly what equities needed.

From there the rotation almost wrote itself. Lower oil eased inflation expectations, which eased pressure on long-duration assets, which freed up the exact parts of the market that had been most punished in March. Oracle popped roughly 13% on Monday on AI platform news. ServiceNow and Ares Management each jumped mid-single-digits. Nvidia, remarkably, stitched together its longest daily winning streak on record. In a week, the market relearned a lesson it had clearly forgotten: the stocks that hurt the most on the way down are often the same ones that move the most on the way back.

The obvious caveat sits right at the door. The ceasefire is two weeks. Israeli ministers are reportedly “outraged” by it. Iran’s Parliament Speaker said Tehran would approach it “with caution.” And Cleveland Fed’s Mester was on the tape Friday saying she’s still modeling scenarios where inflation pushes higher because of the war. The off-ramp is real. So is the on-ramp back. For diversified portfolios, this week was a reminder that the value of staying invested through a scary tape shows up in weeks exactly like this one — and that the hedges you wish you hadn’t bought in March are the same hedges you’ll be glad you kept if the truce breaks.

From Around the Watercooler

Madison Air Jumps After Biggest US Industrial IPO Since 1999

TSMC first-quarter profit rises 58%, beats estimates as AI demand fuels record run

The Starship V3 static fire everyone was waiting for just happened

S&P 500 posts new record close, Nasdaq notches longest win streak since 2009

Disclousure:

Investing involves risk, including the possible loss of principal and fluctuation of value. Past performance is no guarantee of future results.

This newsletter is not intended to be relied upon as forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date noted and may change as subsequent conditions vary. The information and opinions contained in this letter are derived from proprietary and nonproprietary sources deemed by Waterloo Capital to be reliable. The letter may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projection, and forecasts. There is no guarantee that any forecast made will materialize. Reliance upon information in this letter is at sole discretion of the reader. Please consult with a Waterloo Capital financial advisor to ensure that any contemplated transaction in any securities or investment strategy mentioned in this newsletter aligns with your overall investment goals, objectives and tolerance for risk. Additional information about Waterloo Capital is available in its current disclosure documents, Form ADV, Form ADV Part 2A Brochure, and Client Relationship Summary report which are accessible online via the SEC’s investment Adviser Public Disclosure (IAPD) database at www.adviserinfo.sec.gov, using SEC # 133705. Waterloo Capital is neither an attorney nor an accountant, and no portion of this content should be interpreted as legal, accounting or tax advice.