S&P 500: -2.02% DOW: -3.01% NASDAQ: -1.24% 10-YR Yield: 4.12%

What Happened?

Wall Street rode a volatile rollercoaster this week as escalating conflict with Iran sent oil prices soaring and major indexes whipsawing through dramatic intraday swings. All three major U.S. indices ultimately finished the week in the red as earlier rebound attempts faded into risk-off positioning. It was a tale of two markets: energy stocks are leading 2026 with outsized year-to-date gains as crude trades in the mid‑$80s per barrel, while tech has stumbled under the weight of massive AI infrastructure spending plans and growing investor skepticism about near‑term returns. Microsoft’s latest quarter captured that tension perfectly; revenue climbed to $81.3 billion (up 17% year-over-year) with Azure growing 39%, but the stock sold off as investors balked at record $37.5 billion in capital expenditures tied to AI build‑out.

The week’s drama peaked when South Korea’s Kospi plunged in double digits intraday, its worst drop on record, before U.S. markets clawed back from session lows. Energy Select Sector SPDR (XLE) has emerged as 2026’s early standout as money rotates out of crowded AI winners and into cash‑flowing, commodity‑linked names and other defensive plays. The real story: markets are moving from unbridled AI optimism to a more conditional phase, where spending without clear monetization gets punished even as Big Tech doubles down on data centers. With Fed rate‑cut expectations drifting toward mid‑year and a fresh geopolitical risk premium now embedded in oil and shipping, March is already signaling that 2026 could be a bumpier ride than the last leg of the bull market.

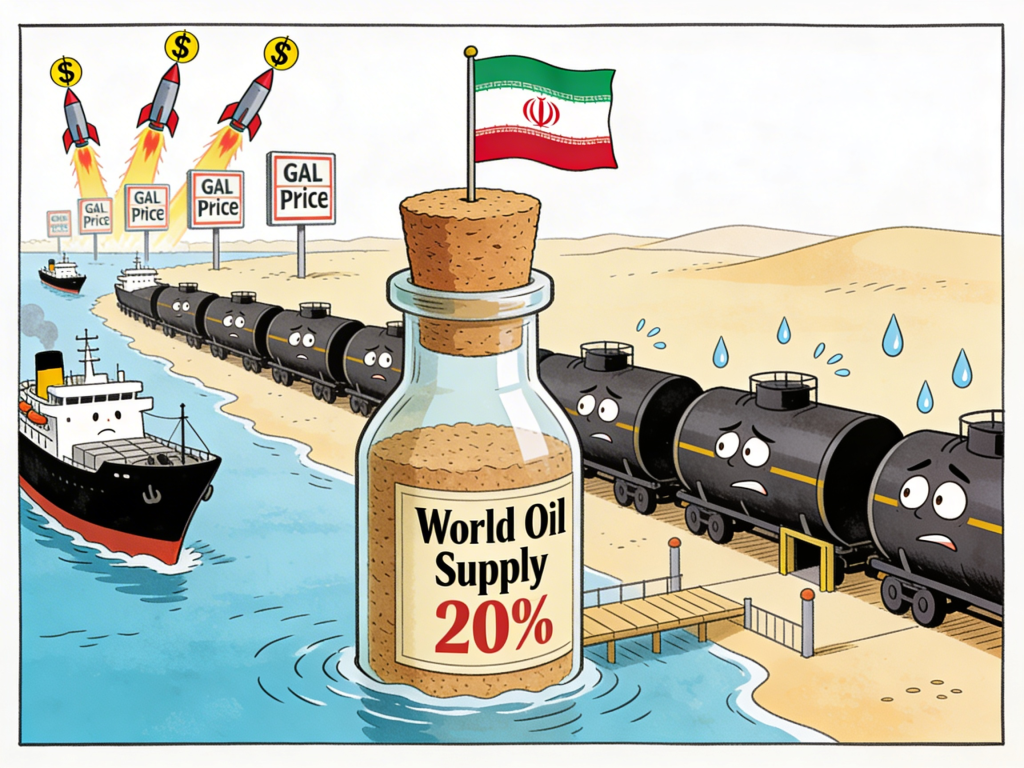

Kuwait Cuts Oil Production as Fallout From Iran Conflict Intensifies

- Brent crude rose 13% early Tuesday to $85/barrel, marking the highest level since January 2025.

- U.S. gasoline prices exceeded $3/gallon nationally while European diesel futures hit $1,130/tonne, the highest since October 2022, as refineries faced acute supply shortages.

The key takeaway – The Strait of Hormuz, the 21-mile-wide chokepoint handling 20% of global oil supply, became ground zero for market chaos this week as U.S.-Israeli strikes on Iran triggered swift retaliation. Tehran’s threat to target any vessel passing through the strait effectively closed shipping lanes, leaving tankers stranded and refineries scrambling for alternative crude sources. Brent crude exploded 13% in early trading Tuesday, briefly topping $85/barrel before settling at $84.04 by week’s end, a five-day winning streak.

The ripple effects hit hard and fast. Iraq, OPEC’s second-largest producer, warned output could drop 3 million barrels per day within days, while Qatar halted gas production and Saudi refineries went dark. U.S. gasoline prices blew past $3/gallon for the first time since early 2025, handing the administration a political headache heading into midterms. Heavy crude from the Americas saw prices surge to multi-year highs, Mars sour crude traded at a $5.50 premium over WTI, its strongest since April 2020, as refiners in India, South Korea, and China pivoted away from Middle Eastern supply.

But here’s the twist: despite the supply shock, oil hasn’t cracked $100 yet. Analysts at RBC Capital Markets note prices are “lagging as an indicator,” suggesting traders believe the U.S. military won’t allow Hormuz to stay blocked long-term. JP Morgan estimates that if the strait remains closed through day eight, crude supply could fall by 4.3 million barrels daily. Meanwhile, diesel futures jumped 10% to $3.60/gallon as European markets hit their highest levels since October 2022. The energy sector’s 21.5% YTD surge now looks justified, but only if tensions don’t escalate further. Venezuela’s 19.4 billion barrels suddenly look very attractive.

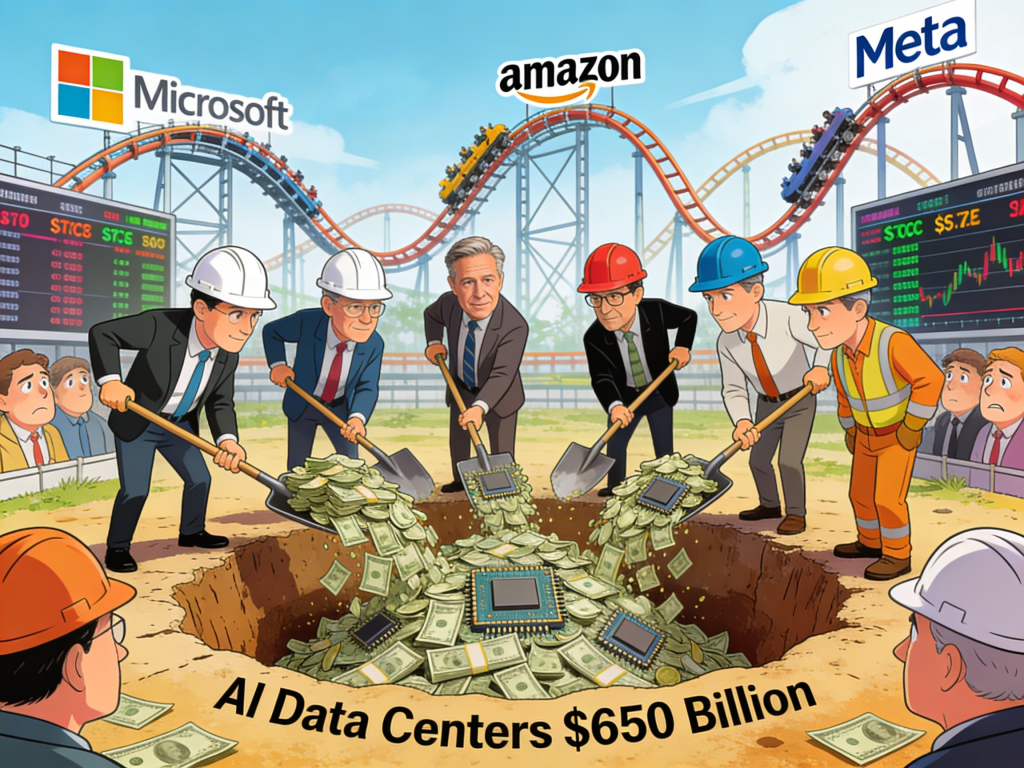

Why Larry Ellison’s US tech giant is cutting thousands of jobs

- The four major hyperscalers are forecast to spend $635-665 billion combined in 2026, representing a 67-74% increase from 2025’s $381 billion.

- Microsoft reported $81.3 billion quarterly revenue (+17% YoY) and $38.5 billion profit (+60% YoY), with Azure cloud growing 39%, yet shares fell 11% as investors questioned $37.5 billion quarterly capex.

The key takeaway – The AI arms race just went thermonuclear. Alphabet, Amazon, Meta, and Microsoft collectively unveiled plans to spend between $635-665 billion on AI infrastructure in 2026, a staggering 67% increase from 2025’s record $381 billion. Amazon leads the pack with $200 billion earmarked for data centers and chips, followed by Alphabet’s $175-185 billion, Meta’s $115-135 billion range, and Microsoft’s $145 billion run rate. To put it in perspective: that’s $1.8 billion per day, more than Walmart’s entire 2025 revenue, and roughly 25% of global military spending.

But Wall Street isn’t buying the hype, yet. Amazon’s stock tanked 8% after its spending reveal, Alphabet dropped 3%, and Microsoft cratered 11% despite posting a 60% profit jump and $81.3 billion in quarterly revenue. The only winner? Meta, whose shares surged as AI-driven ad revenue proved the monetization case. Investors have shifted from blind enthusiasm to demanding proof of returns, creating what DA Davidson analyst Gil Luria calls “a very healthy level of caution—probably more than any cycle I’ve seen.”

The divergence is stark. While hyperscalers hemorrhage cash on infrastructure, chip makers are printing money; Nvidia, Broadcom, and AMD shares jumped 5-6% on Amazon’s announcement. Meanwhile, the broader tech sector is down 3% YTD, with the Magnificent Seven sliding 8.8% as AI fatigue sets in. Morgan Stanley analysts expect Alphabet alone could hit $250 billion in capex by 2027, but questions linger: When do these investments pay off? Can Azure sustain 39% growth? And is this bubble territory? The market’s message is clear, show us the money, or expect more pain. For now, Big Tech is building the biggest bet in corporate history. Just don’t expect investors to applaud until revenue catches up.

From Around the Watercooler

How the Dash to Collect Tariff Refunds Will Play Out

U.S. Retail Sales Sagged in January

Six Flags to Sell 7 of Its Amusement Parks

Private companies added 63,000 jobs in February, January revised to just 11,000 additions

Disclousure:

Investing involves risk, including the possible loss of principal and fluctuation of value. Past performance is no guarantee of future results.

This newsletter is not intended to be relied upon as forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date noted and may change as subsequent conditions vary. The information and opinions contained in this letter are derived from proprietary and nonproprietary sources deemed by Waterloo Capital to be reliable. The letter may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projection, and forecasts. There is no guarantee that any forecast made will materialize. Reliance upon information in this letter is at sole discretion of the reader. Please consult with a Waterloo Capital financial advisor to ensure that any contemplated transaction in any securities or investment strategy mentioned in this newsletter aligns with your overall investment goals, objectives and tolerance for risk. Additional information about Waterloo Capital is available in its current disclosure documents, Form ADV, Form ADV Part 2A Brochure, and Client Relationship Summary report which are accessible online via the SEC’s investment Adviser Public Disclosure (IAPD) database at www.adviserinfo.sec.gov, using SEC # 133705. Waterloo Capital is neither an attorney nor an accountant, and no portion of this content should be interpreted as legal, accounting or tax advice.