S&P 500: 1.07% DOW: 0.25% NASDAQ: 1.51% 10-YR Yield: 4.09%

What Happened?

A mixed bag of returns this week left major indices grinding for gains, as markets digested a mixed bag of macro headlines, geopolitics, and an earnings season that refused to tell a single clean story. Oil moved higher as renewed tensions between the U.S. and Iran pushed risk premia back into energy markets, offering a tailwind to energy names while simultaneously reviving old concerns about input costs and inflation pressure. That backdrop kept the broader tape choppy: cyclical sectors traded on growth and commodity narratives, while rate‑sensitive and long‑duration corners of the market continued to trade every macro headline like a live grenade.

On the policy front, the U.S. Supreme Court’s ruling that President Trump’s sweeping “blanket” tariffs were unlawful added an eleventh‑hour twist to the week. Earnings, meanwhile, have done little to provide a clear directional anchor. Materials and select cyclicals managed to outperform on the back of better pricing power and commodity leverage, but the tone across reports has been one of “beats with caveats” rather than unambiguous strength. Many companies cleared the bar on the quarter just reported, yet guidance and outlook commentary were all over the map: some management teams leaned into resilient demand and easing cost pressures, while others flagged margin compression, slower volumes, or lingering uncertainty around policy and geopolitics. The net effect for indices was more rotational than directional, as capital continued to shuffle between sectors and styles in search of earnings durability, but without the kind of unified earnings or macro narrative needed to push markets decisively higher or lower in one shot.

Fed Minutes Reveal Little Appetite for Rate Cuts

- Fed Minutes showed very little appetite for interest rate cuts at their previous meeting.

- Previous meeting in late January held rates steady for first time since July.

The key takeaway – For the past 6 months, the Federal Reserve has essentially been playing defense, issuing insurance cuts to protect against a weakening labor market. However, the newly released January minutes signal a definitive shift in strategy as the committee hits the pause button. While officials acknowledge the labor market’s underlying fragility, they are now more concerned with persistent price pressures, warning that progress toward their 2% target might be “slower and more uneven” than many had hoped. This cautious stance was only reinforced by the strong January jobs report, which saw a 130,000 job print that effectively cooled the urgency for further immediate cuts.

With inflation still hovering around 2.5%, the Fed is likely moving away from preemptive strikes and back to a strictly data-dependent approach, content to wait for clearer signs of either a labor market crack or a sustained inflationary dip before making their next move. Ultimately, this “higher for longer” posture suggests that relief for mortgage rates and consumer borrowing costs may remain on the horizon rather than arriving in the immediate weeks to months ahead.

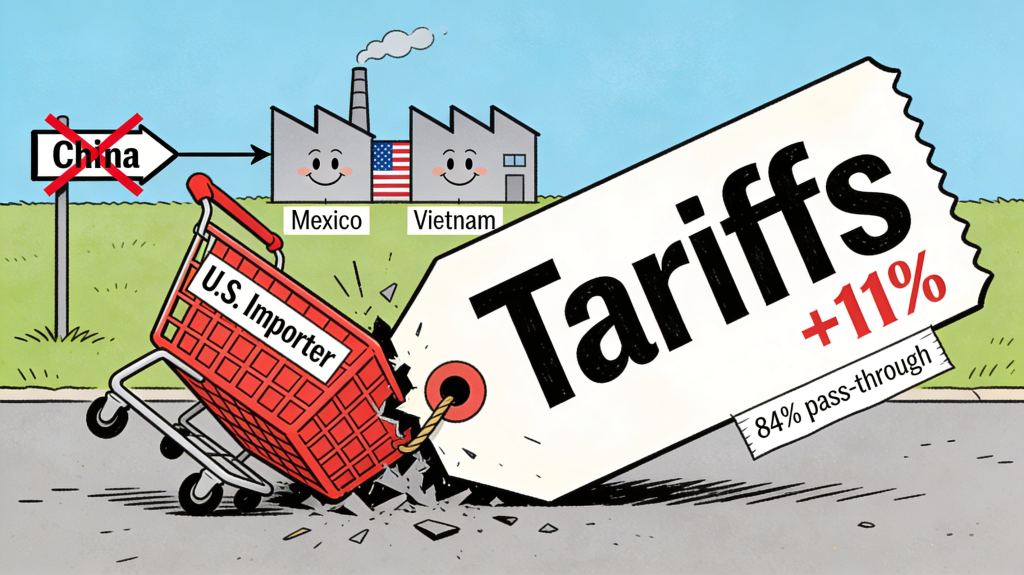

What to Know About the Supreme Court Ruling on Trump’s Tariffs

- U.S. importer pass-through was approximately 84% as of November 2025, indicating most tariff costs were borne domestically.

- The average cost of U.S. imported goods subject to tariffs rose about 11%.

- Supply chains continued to diversify away from China, with Vietnam and Mexico gaining share as key alternative sourcing hubs.

The key takeaway – Tariffs were back in the spotlight last week as fresh data underscored how protectionism has been acting as a tax on U.S. businesses and consumers, and the Supreme Court simultaneously moved to clip the White House’s authority to keep pushing that trend. With average tariffs hovering around the low-teens, U.S. import prices on covered goods have risen by roughly a similar magnitude, confirming that the bulk of the cost has been passed through to domestic importers rather than absorbed offshore. At the same time, years of elevated duties have visibly reshaped trade flows: China’s share of U.S. imports has fallen from roughly a quarter of the total to below 10%, while countries like Mexico and Vietnam have stepped into the gap as alternative production hubs.

The new twist is legal rather than economic: the Supreme Court has now ruled that President Trump’s broad “reciprocal” tariffs exceeded his statutory authority, effectively striking down some of the most sweeping measures and forcing any future tariffs back into narrower, more clearly defined legal channels. For markets, that creates a nuanced setup. On one hand, the decision reduces the tail risk of ever-escalating unilateral tariffs that could have further squeezed margins, weighed on global trade volumes, and pressured risk assets. On the other, it injects uncertainty around what the replacement regime will look like and whether Congress will move to reassert itself on trade. For major indices, the macro read-through is cautiously constructive at the margin: less legal room for surprise tariffs supports valuations for globally exposed sectors, but investors should expect ongoing volatility as policy is reworked and companies reassess supply chains in a world where trade strategy is now constrained not just by economics and politics, but by the courts as well.

From Around the Watercooler

Seattle Seahawks begin sale process after Super Bowl win

Trump says he’s considering limited military strike against Iran

Equinox’s $40,000-a-year membership has a waiting list

How Streaming Became Cable TV’s Unlikely Life Raft

Disclousure:

Investing involves risk, including the possible loss of principal and fluctuation of value. Past performance is no guarantee of future results.

This newsletter is not intended to be relied upon as forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date noted and may change as subsequent conditions vary. The information and opinions contained in this letter are derived from proprietary and nonproprietary sources deemed by Waterloo Capital to be reliable. The letter may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projection, and forecasts. There is no guarantee that any forecast made will materialize. Reliance upon information in this letter is at sole discretion of the reader. Please consult with a Waterloo Capital financial advisor to ensure that any contemplated transaction in any securities or investment strategy mentioned in this newsletter aligns with your overall investment goals, objectives and tolerance for risk. Additional information about Waterloo Capital is available in its current disclosure documents, Form ADV, Form ADV Part 2A Brochure, and Client Relationship Summary report which are accessible online via the SEC’s investment Adviser Public Disclosure (IAPD) database at www.adviserinfo.sec.gov, using SEC # 133705. Waterloo Capital is neither an attorney nor an accountant, and no portion of this content should be interpreted as legal, accounting or tax advice.